Our editorial team follows strict guidelines to ensure accuracy and objectivity. Learn more about our process.

Alabama home insurance pays to repair or rebuild your house, replace belongings, cover liability, and fund extra living costs after a covered loss. Rates swing by county, roof age, and distance to the Gulf. Hurricane and tropical-storm risk matters on the coast; tornado and hail risk matters statewide. Mortgage lenders expect proof of insurance at closing; even without a loan, dwelling and liability limits deserve a real review. Alabama home insurance quotes should be judged on matching dwelling limit and deductibles—including any named-storm or wind or hail deductibles—not on a cheap headline alone.

Average Cost of Home Insurance in Alabama

Premiums vary widely, but many Alabama homeowners land around $1,300–$2,200+ per year for a typical home with common limits—often about $110–$185 per month if you spread the annual bill evenly. Coastal counties and high-tornado corridors can sit well above that band; every risk is priced on its own.

Insurers use approved rating factors including credit where state law allows, along with replacement cost, location, roof age, and claims history.

| Approx. dwelling limit (Coverage A) | Typical annual premium range |

|---|---|

| $300,000–$400,000 | Often $1,100–$2,000+ |

| $400,000–$600,000 | Often $1,600–$3,200+ |

| $600,000+ | Often $2,200+ (coastal or high-hazard ZIPs can be higher) |

| Area | What often moves the number |

|---|---|

| Birmingham / central AL | Tornado, hail, urban rebuild cost |

| Mobile / Gulf Coast | Hurricane wind, named-storm deductibles, flood gap |

| Huntsville / north | Severe storms, hail |

| Montgomery / south-central | Wind, hail, river flood exposure |

Best Home Insurance Companies in Alabama

Carriers writing or supporting business in Alabama often include State Farm, Allstate, Farmers, Nationwide, Travelers, and Liberty Mutual, among others—appetite changes by ZIP and year. Coastal homes may need wind or flood layers beyond a standard HO-3; ask a licensed agent about residual or coastal markets if voluntary carriers tighten.

Home Insurance Challenges in Alabama

Hurricane and tropical-storm exposure on the Gulf drives wind and water claims; named-storm or percentage deductibles are common on the coast. Inland hail and tornado outbreaks can spike roof and exterior claims. Flood from rising water is not covered under a standard homeowners policy—use NFIP or private flood where you need it. Voluntary carriers sometimes reduce appetite after big storm years; work with a licensed agent if non-renewal or coastal eligibility becomes an issue.

Expert Tip: Coastal Wind and Flood Are Different Perils

Wind-driven rain and storm surge are not the same as rising-water flood. Read your declarations page for named-storm deductibles and flood exclusions. If you are in a surge-prone zone, model flood coverage with a licensed agent—not just the homeowners premium.

—Brad Cummins

How to Get Home Insurance Quotes in Alabama

- Align the snapshot: gather year built, roof age and material, square footage, and safety features (smoke alarms, monitored alarm, and wind mitigation where it applies).

- Request quotes from multiple companies (or have a licensed agent shop appointed carriers for you). Alabama home insurance quotes should use the same dwelling limit and deductibles so you are not mixing apples and oranges.

- Review coverage, not just price: check dwelling, other structures, personal property, loss of use, and liability; read endorsements that match Gulf or tornado exposure.

- Check eligibility for coastal or high-hazard zones—some risks route to a residual market or specialty carrier.

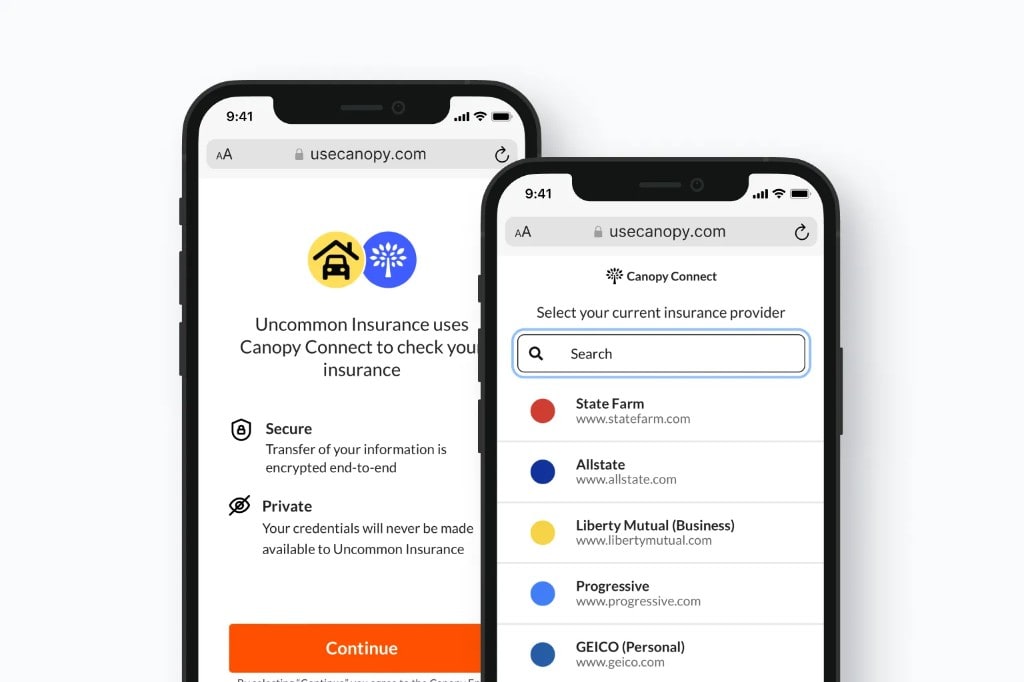

- If you already have a policy, you can securely connect it through our flow to import your declarations page and shop the same coverage stack with appointed carriers.

What Homeowners Insurance Covers

A standard HO-3 form covers the dwelling on an open-peril basis (subject to exclusions) and belongings on named perils—see home insurance perils for how your form lists events. The home insurance coverages hub breaks down each part in plain language:

- Dwelling coverage (Coverage A) — Structure and attached components; set limits to rebuild, not market value.

- Other structures (Coverage B) — Detached garage, fence, shed—often a percentage of Coverage A.

- Personal property (Coverage C) — Belongings; schedule jewelry or art if needed.

- Loss of use (Coverage D) — Extra costs if you cannot live at home during a covered repair.

- Personal liability (Coverage E) — Injury and property damage you are legally responsible for.

ACV vs replacement cost explains how claim payments are calculated.

What Homeowners Insurance Does Not Cover

- Flooding from storms, rivers, or mudslides — Separate flood coverage; review sewer and water backup where offered.

- Earthquake — Earthquake policy or endorsement where you need it.

- Maintenance and wear — Not a covered peril.

Keep your declaration page with evacuation and rebuild plans.

Why Home Insurance Is Expensive in Alabama

Catastrophe exposure (hurricane, tornado, hail), reinsurance costs, and higher rebuild and labor costs in growing metros push replacement cost estimates—and premiums—upward. Coastal wind modeling and litigation trends can also influence filings. Carrier appetite shifts after large events, which shows up in renewals.

Get Free Alabama Home Insurance Quotes

As a licensed independent agency, we shop rates from multiple home insurance carriers so you can see who offers the best price for your coverage. You can start a quote or securely connect your current policy to review premiums, limits, and deductibles side-by-side before making a change.

Don't have time to run a quote? Just send us your policy

Share your current policy declarations pages with us in two clicks. Takes about 30 seconds. We'll review your coverage, find gaps, and compare our carriers to your current policy.

Connect your policy

FAQ

About Brad Cummins

Brad Cummins is the founder of Insurance Geek and primary author of its educational content. Licensed since 2004, he brings over 21 years of experience structuring life insurance and IUL strategies for clients nationwide.

Fact checked by Brianna Baiocco

Brianna Baiocco runs P&C operations at Insurance Geek and fact-checks property and casualty content. Licensed since 2009, she brings over 16 years of experience in auto, home, renters, and commercial insurance.