Our editorial team follows strict guidelines to ensure accuracy and objectivity. Learn more about our process.

Vermont renters insurance costs $12-17 monthly for most renters, protecting your belongings from theft, fire, and winter weather damage. Whether you're in Burlington, Bennington, or Rutland, coverage is affordable and often required by landlords.

At Insurance Geek, you can get real quotes and bind coverage today through our direct partnerships with Assurant, SafeCo, Nationwide, and Progressive. No lead generation runaround—actual coverage you can start immediately.

How Much Does Renters Insurance Cost in Vermont?

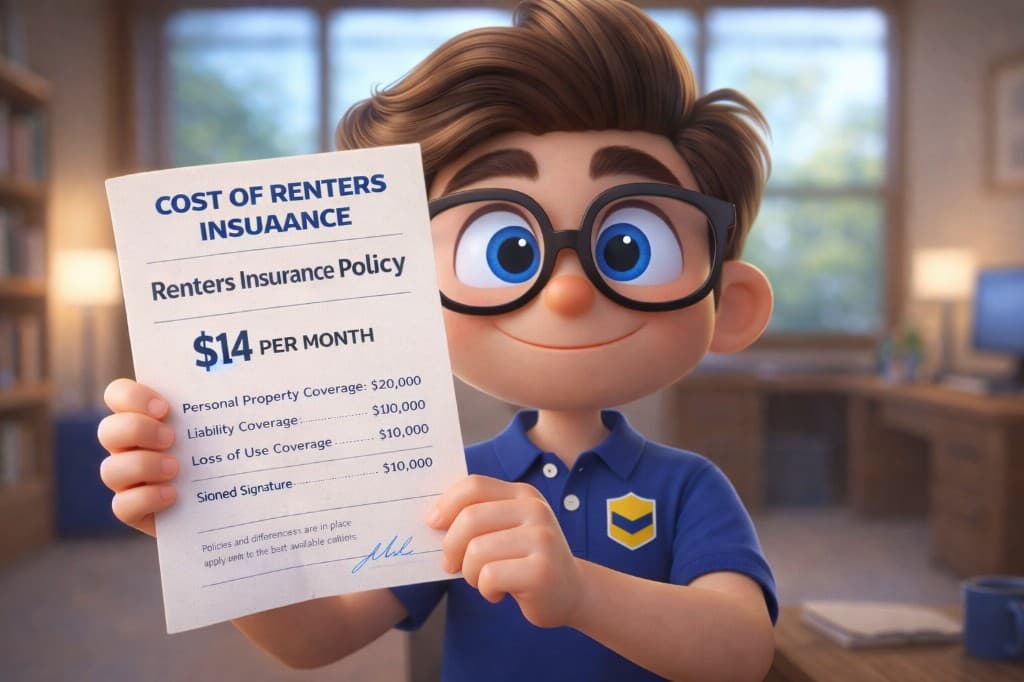

Most Vermont renters pay between $12-17 per month for coverage, making it one of the most affordable states in the country. Your exact cost depends on your location, coverage amount, and deductible choice.

Vermont City Cost Breakdown

Renters insurance costs vary across the state based on local risk factors:

Burlington: $14-18/month—higher rates reflect urban density and property values Bennington: $13-16/month—moderate pricing for southwestern Vermont Rutland: $12-15/month—affordable rates in central Vermont South Burlington: $14-17/month—similar to Burlington metro pricing Essex Junction: $13-16/month—competitive rates near Burlington

Rural areas typically see lower rates due to reduced theft risk and lower property values. Mountain communities near ski resorts sometimes pay slightly more due to winter weather exposure.

What Affects Your Rate?

- Coverage amount determines your base premium—most policies start at $20,000 personal property coverage

- Deductible choice impacts monthly cost—$500 deductibles cost more than $1,000 deductibles

- Location and ZIP code reflect local crime rates and weather risks

- Claims history affects eligibility and pricing—clean records get better rates

What Does Vermont Renters Insurance Cover?

Standard Vermont renters insurance provides three main protections for your apartment or rental home.

Your Belongings

Personal property coverage protects everything you own—furniture, electronics, clothing, and appliances. If your stuff gets stolen or damaged by fire, your policy pays to replace it up to your coverage limit. This protection extends beyond your apartment, covering items in your car or storage unit.

Liability Protection

Liability coverage kicks in when someone gets hurt in your rental or you accidentally damage the property. If a guest slips on your stairs or your kitchen fire spreads, the policy covers legal fees and medical bills. Most policies start at $100,000 liability, but you can increase it to $300,000 or $500,000 for minimal additional cost.

Temporary Housing

Loss of use coverage pays hotel bills and extra living costs if your rental becomes uninhabitable. After a fire or major damage, your policy covers the difference between your normal rent and temporary housing expenses while repairs happen.

Vermont Weather Risks

Vermont's harsh winters create unique coverage needs. Standard policies cover damage from frozen pipes, ice dams, heavy snow, and blizzards. However, flood damage requires separate coverage—particularly important if you're in Washington County, Windsor County, or Lamoille County where flooding occurs most frequently.

Ice storms cause significant damage when freezing rain weighs down power lines and trees. Your policy covers property damage from falling branches or power outages, though extended food spoilage from outages may have limited coverage.

How to Buy Renters Insurance in Vermont

Getting covered takes just a few steps when you work with the right provider.

Calculate Your Coverage Needs

Walk through your apartment and estimate what it would cost to replace everything. Most renters need $20,000-40,000 in personal property coverage. Don't forget items in storage, your car, or at friends' places—your policy covers possessions anywhere in the world.

Choose Your Deductible

Your deductible is what you pay before insurance kicks in. A $500 deductible costs more monthly but saves money on small claims. A $1,000 deductible lowers your premium but means you cover more damage yourself. Most Vermont renters choose $1,000 deductibles to balance affordability and coverage.

Consider Bundling Discounts

Combining renters and auto insurance typically saves 15-25% on both policies. If you're already insured for your car, check if the same company offers renters coverage. The discount often makes renters insurance essentially free.

Look for Additional Discounts

Vermont insurers offer savings for protective devices like smoke detectors and deadbolts. Some provide discounts for paying annually instead of monthly, or for going paperless. Ask about multi-policy, claims-free, and protective device discounts when getting quotes.

Do You Need Renters Insurance in Vermont?

Vermont law doesn't require renters insurance, but your landlord probably does. Most lease agreements in Burlington, Bennington, and Rutland require proof of coverage before move-in, typically with at least $100,000 liability protection.

Even without a requirement, coverage makes financial sense. Replacing your belongings after a fire or theft could cost $20,000-50,000. For $12-17 monthly, you protect everything you own and shield yourself from liability lawsuits if someone gets hurt in your rental.

Vermont's winter weather creates additional risks. Frozen pipes can burst and flood your apartment. Heavy snow can collapse roofs or damage windows. Ice storms can knock out power for days. Without coverage, you're financially exposed to these common Vermont risks.

Get a Vermont renters insurance quote fast

Ready to see your Vermont renters insurance price? Run your quote online and get covered in minutes.

Get renters insurance in under 2 minutes

See your price, choose coverage, and download proof instantly. Get your policy now.

Frequently Asked Questions

About Brad Cummins

Brad Cummins is the founder of Insurance Geek and primary author of its educational content. Licensed since 2004, he brings over 21 years of experience structuring life insurance and IUL strategies for clients nationwide.

Fact checked by Brianna Baiocco

Brianna Baiocco runs P&C operations at Insurance Geek and fact-checks property and casualty content. Licensed since 2009, she brings over 16 years of experience in auto, home, renters, and commercial insurance.