Our editorial team follows strict guidelines to ensure accuracy and objectivity. Learn more about our process.

Washington DC renters insurance protects your personal belongings and provides liability coverage for just $14-21 per month on average. With over 280,000 renters in the District and property crime rates of 41 per 1,000 residents, having coverage is essential protection against theft, fire, and water damage that your landlord's policy won't cover.

Unlike many states, the District of Columbia doesn't require renters insurance by law, but most landlords do. Nearly 42% of DC residents rent their homes, yet only 44% carry renters insurance, leaving thousands exposed to significant financial risk. Understanding your coverage options and costs can help you make an informed decision about protecting your belongings in the nation's capital.

How Much Does Renters Insurance Cost in Washington DC?

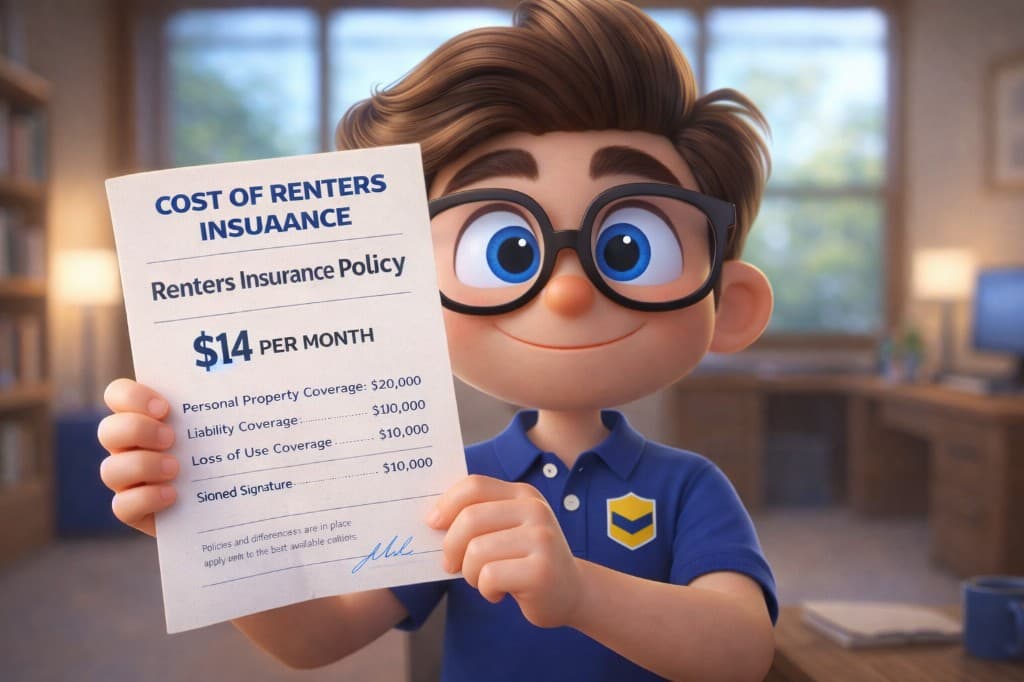

Renters insurance in Washington DC costs an average of $14-21 per month or $168-252 annually, depending on your coverage limits and the insurance company you choose. This makes DC slightly more affordable than the national average of $22 per month.

| Insurance Geek Partners | Key Benefit | Best For |

|---|---|---|

| Assurant | Instant quote & bind | Immediate coverage needs |

| SafeCo | Affordable rates | Bundling discounts & savings |

| Branch Insurance | Digital innovation | Tech-savvy professionals |

| Nationwide | Comprehensive coverage | Robust protection & value |

| Progressive | Bundling flexibility | Multi-policy convenience |

While digital insurers like Lemonade have gained attention in DC for convenience, Insurance Geek's partnerships provide superior advantages including instant binding through Assurant's API integration, better bundling discounts, and real agency expertise that digital-only platforms cannot match. Military families may find specialized rates through USAA, but for most DC renters, our partner carriers offer the best combination of speed, affordability, and comprehensive coverage.

What Does Renters Insurance Cover in Washington DC?

DC renters insurance provides four main types of coverage that protect both your property and your financial well-being:

Personal Property Coverage

This covers your belongings against covered perils like fire, theft, vandalism, and water damage from burst pipes. Your policy protects items both inside your rental unit and when you're traveling. Most policies cover personal property on a replacement cost basis, meaning you receive enough money to buy new items rather than their depreciated value.

Common covered items include furniture, electronics, clothing, appliances, and sporting equipment. High-value items like jewelry or art may require additional coverage through scheduled personal property endorsements.

Liability Protection

Personal liability coverage protects you if someone is injured in your rental unit or if you accidentally damage someone else's property. In DC, most landlords require at least $100,000 in liability coverage, though many insurance experts recommend $300,000 or more given the area's high income levels and potential lawsuit costs.

This coverage also includes legal defense costs if you're sued, which can be substantial in the DC metropolitan area where legal fees tend to be higher than the national average.

Additional Living Expenses

If your rental becomes uninhabitable due to a covered loss, this coverage pays for temporary housing, meals, and other necessary expenses while repairs are made. Given DC's high cost of living and limited hotel availability, this coverage can be particularly valuable for District renters.

Medical Payments Coverage

This covers minor medical expenses for guests injured in your rental, typically ranging from $1,000 to $5,000. It applies regardless of fault and can help avoid larger liability claims.

Expert Tip: DC-Specific Coverage Considerations

DC renters should pay special attention to water damage coverage. Many older buildings in areas such as Capitol Hill and Dupont Circle have aging plumbing systems that can lead to significant water damage. Standard policies cover sudden water damage but not gradual leaks or flooding.

—Brad Cummins, Insurance Geek Founder

What Renters Insurance Doesn't Cover in DC

Understanding coverage exclusions is crucial for DC renters, especially given the area's unique risks:

Flood Damage

Standard renters insurance typically doesn't cover flooding, which can be a concern in DC due to its proximity to the Potomac River and the occasional heavy rainfall that can overwhelm storm drainage systems. Renters in flood-prone areas should consider separate flood insurance through the National Flood Insurance Program.

Earthquake Damage

Although earthquakes are rare in the DC area, they can still occur. The 2011 Virginia earthquake, which affected the DC area, reminded residents that seismic activity is a possibility. Most standard policies exclude earthquake damage.

Roommate's Belongings

Your policy only covers your personal property. Each roommate needs their own renters insurance policy to protect their belongings. This is particularly important in DC where many young professionals share apartments to manage high housing costs.

Business Property

If you work from home, your renters insurance typically provides limited coverage for business equipment. Given DC's large population of consultants, freelancers, and remote workers, consider adding business property coverage if you have expensive work equipment.

DC Renters Insurance Requirements

While Washington DC doesn't legally require renters insurance, the practical reality is quite different:

Landlord Requirements

Most DC landlords require renters insurance as a lease condition. Common requirements include:

- Minimum $100,000 liability coverage (some require $300,000)

- Landlord listed as "additional interested party" on the policy

- Proof of coverage before move-in and at lease renewal

- Continuous coverage throughout the lease term

Property management companies often offer resident benefits packages that automatically include renter's insurance, typically costing $25-$ 40 per month. While convenient, these policies may be more expensive than shopping independently and might provide limited coverage options.

Condo and Co-op Considerations

If you're renting a condo or co-op in DC, it's essential to understand that the building's master policy typically only covers common areas and the building's structure. Your renters' policy needs to cover interior improvements, personal property, and liability within your unit.

Best Renters Insurance Companies for DC Residents

Insurance Geek partners with top-rated carriers to offer DC renters fast and competitive coverage options. While Lemonade has gained popularity in DC for its digital approach, our direct partnerships offer superior advantages, including instant binding and real agency expertise.

Assurant

Best for: Instant coverage and immediate binding

Through Insurance Geek's direct API integration with Assurant, DC renters can get instant quotes and bind coverage in minutes without typical waiting periods. This seamless quote-to-bind process makes getting protected faster and simpler than traditional insurance applications or digital-only platforms like Lemonade that still require processing time. Assurant's streamlined approach is perfect for busy DC professionals who need immediate coverage.

SafeCo

Best for: Affordability and bundling discounts

SafeCo consistently offers some of the most affordable renters insurance for DC residents, with excellent bundling opportunities that often outperform popular options, such as Lemonade's standalone policies. If you already have auto insurance, adding a SafeCo renters policy can lead to significant savings on both policies. Their claims-free discount rewards customers who maintain a clean claims history, making them ideal for responsible renters.

Branch Insurance

Best for: Digital innovation and community benefits

As a digital-first insurer, Branch offers competitive rates for DC renters, complemented by an innovative community-based approach that surpasses what traditional digital platforms provide. Their platform provides discounts that improve as more people in your network join, and their streamlined mobile app handles everything from quotes to claims, making them ideal for tech-savvy DC professionals seeking more than basic digital coverage.

Nationwide

Best for: Comprehensive coverage and reliability

Nationwide provides excellent value for DC renters seeking robust coverage, along with valuable add-ons like Brand New Belongings coverage. Their multi-policy discounts are among the most generous available, making them particularly affordable when bundled with auto insurance. Their long-standing reputation provides peace of mind that newer digital-only platforms may not offer.

Progressive

Best for: Bundling flexibility and competitive rates

Progressive offers DC renters excellent bundling opportunities and competitive standalone rates. Their flexible coverage options and multi-policy discounts make them particularly attractive for renters who want the convenience of having multiple insurance products with one established carrier, providing stability that digital startups cannot guarantee.

How to Buy Renters Insurance in Washington DC

Follow these steps to secure the best renters insurance for your DC rental:

1. Inventory Your Belongings

Create a detailed list of your personal property and estimate replacement costs. DC renters often underestimate the value of their belongings, particularly electronics, clothing, and kitchen items. Use smartphone apps to photograph each room and keep receipts for major purchases.

2. Determine Coverage Needs

Most DC renters require $25,000-$ 50,000 in personal property coverage. Consider your lifestyle: young professionals with basic furnishings might need less coverage, while established renters with expensive electronics and furniture require more.

For liability coverage, consider DC's high-income demographics and potential exposure to lawsuits. While landlords typically require $100,000, many insurance experts recommend $300,000 for better protection.

4. Compare Multiple Quotes

Get instant quotes through Insurance Geek's direct Assurant integration, or compare options from our other partner carriers - SafeCo, Branch Insurance, Nationwide, and Progressive. Our comparison technology helps you evaluate coverage options to find what best fits your needs and budget, with the ability to bind immediately through Assurant's API integration.

5. Ask About Discounts

DC renters can save money through various discounts available from our partner carriers:

- Multi-policy discount: Bundle with auto insurance for 10-25% savings

- Security features: Discounts for burglar alarms, doormen, or gated communities

- Claims-free discount: Lower rates for maintaining a clean claims history

- Loyalty discount: Reduced rates after several years with the same insurer

6. Review Policy Details

Before purchasing, carefully review coverage limits, deductibles, and exclusions. Pay particular attention to coverage for expensive items, such as laptops, phones, and professional equipment commonly used by DC's workforce.

DC Neighborhood Considerations

Your specific DC neighborhood can impact both your insurance needs and rates:

Capitol Hill

Historic rowhouses with older plumbing and electrical systems may be at a higher risk of water damage and fire hazards. Consider higher personal property limits and ensure coverage for period-appropriate fixtures if you've made improvements.

Dupont Circle

Higher property values and income levels in this area suggest carrying higher liability limits. The area's walkability also means higher risk of personal liability incidents.

Columbia Heights

This rapidly gentrifying area has seen a decrease in crime rates, but renters should still ensure adequate theft coverage. The mix of new and older buildings means varying risk profiles.

Georgetown

A premium neighborhood with high property values suggests maximum liability coverage. Historic buildings may have unique risks requiring specialized coverage considerations.

Filing Claims in Washington DC

Understanding the claims process helps ensure smooth resolution when you need coverage:

Immediate Steps After a Loss

Contact your insurance company immediately to report the claim. Most insurers offer 24/7 claim reporting through phone, online portals, or mobile apps. Document damage with photos and create a detailed list of affected items.

For theft claims, file a police report with the Metropolitan Police Department and obtain a copy for your insurance claim. This is particularly important in DC where property crime does occur.

Working with Adjusters

Your insurance company will assign an adjuster to evaluate your claim. Be prepared to provide documentation like receipts, photos, and proof of ownership for valuable items. The adjuster will assess damage and determine coverage under your policy terms.

Temporary Housing

If your rental becomes uninhabitable, your additional living expenses coverage helps pay for temporary accommodations. Keep all receipts for hotels, meals, and other necessary expenses above your normal living costs.

Special Considerations for DC Renters

Student Housing

DC's numerous universities mean many student renters need coverage. Students living in dorms may be covered under parents' homeowners insurance, but those in off-campus housing typically need their own policies. Many insurers offer student discounts or lower coverage limits suitable for typical student belongings.

Short-Term Rentals

If you're staying in DC temporarily for work or an internship, some insurers offer short-term rental policies. However, standard annual policies often provide better value even for shorter stays.

High-Value Items

DC's professional population often owns expensive electronics, jewelry, and professional equipment. Standard policies typically limit coverage for these items, so consider scheduled personal property endorsements for items worth more than $1,000-2,500.

Home-Based Businesses

Many DC residents work as consultants, freelancers, or remote employees. Standard renters' insurance provides limited coverage for business property. If you have expensive work equipment or conduct business from your rental, consider adding business personal property coverage.

Common Renters Insurance Mistakes in DC

Avoid these frequent errors that can leave you underinsured or facing claim denials:

Underestimating Personal Property Value

Many renters significantly underestimate the cost of replacing their belongings. Electronics, clothing, furniture, and kitchen items add up quickly. Use online calculators or work with an agent to determine appropriate coverage limits.

Choosing Actual Cash Value Over Replacement Cost

Actual cash value policies factor in depreciation, potentially leaving you unable to replace damaged items. Replacement cost coverage costs slightly more but provides superior protection.

Ignoring Liability Coverage

Some renters focus solely on personal property coverage and overlook liability protection. Given DC's litigious environment and high-income population, adequate liability coverage is crucial.

Not Reading Policy Exclusions

Understanding what your policy doesn't cover prevents unpleasant surprises during claims. Pay particular attention to flood, earthquake, and business property exclusions.

Get a Washington, D.C. renters insurance quote fast

Ready to see your Washington, D.C. renters insurance price? Run your quote online and get covered in minutes.

Get renters insurance in under 2 minutes

See your price, choose coverage, and download proof instantly. Get your policy now.

Frequently Asked Questions

About Brad Cummins

Brad Cummins is the founder of Insurance Geek and primary author of its educational content. Licensed since 2004, he brings over 21 years of experience structuring life insurance and IUL strategies for clients nationwide.

Fact checked by Brianna Baiocco

Brianna Baiocco runs P&C operations at Insurance Geek and fact-checks property and casualty content. Licensed since 2009, she brings over 16 years of experience in auto, home, renters, and commercial insurance.