Our editorial team follows strict guidelines to ensure accuracy and objectivity. Learn more about our process.

I started IUL policies on both of my kids when they were young — not because they needed life insurance, but because they had something no adult can buy back: time. Decades of tax-deferred compounding, insurability locked in before any health conditions develop, and a tax-free income stream waiting for them at retirement. Below are the real numbers from their actual Allianz policies, including the index credits I locked in for my son in early 2026.

Key Takeaways

A kids IUL locks in guaranteed lifetime insurability at the lowest possible cost. before health conditions can ever disqualify them

Cash value grows linked to a market index with a 0% floor, meaning your child never loses ground in a down market

Funds can be accessed tax-free for college, a home, a business, or anything else. no restrictions, no penalties

Left to grow until retirement, a modest annual premium can generate $200,000+ per year in tax-free income

What Is a Kids IUL?

A kids IUL (Indexed Universal Life) is a permanent life insurance policy issued on a child, owned by a parent or grandparent. The policy builds cash value over time based on the performance of a market index — like the S&P 500 or a custom blended index — subject to a cap and a 0% floor guarantee. That floor is what separates IUL from direct market investing: when the index goes negative, the policy credits zero, not a loss.

The child is the insured. The owner — typically a parent — controls the policy and can transfer ownership to the child at any point. Premiums are typically funded for 20 years, after which the policy sustains itself and continues to grow.

The real advantage of starting at a young age is compound time. A policy started at age 5 or 8 has 57 to 60 years of growth ahead of it before the child reaches 65. That timeline is the engine behind every number on this page. For multi-age illustrated outcomes and retirement income math, see our IUL case studies.

Why Start an IUL for Your Child

Lock In Insurability for Life

The single most undervalued benefit of a kids IUL has nothing to do with money. Once the policy is issued, your child has permanent life insurance coverage no matter what health conditions they develop later. Diabetes, cancer, heart disease — none of it can touch a policy that's already in force. You cannot go back and buy this. You either locked it in early or you didn't.

Tax-Free Access at Any Stage of Life

Unlike a 529 plan that restricts funds to education, or a retirement account that penalizes early withdrawals, an IUL policy lets your child access cash value at any age for any purpose — through policy loans that aren't treated as taxable income by the IRS. College, a first home, seed capital for a business — the policy adapts to whatever their life actually looks like, not what you planned for when they were eight.

Tax-Free Retirement Income

The long game is retirement. A properly structured IUL funded in childhood and left to grow generates a tax-free income stream that would cost far more to replicate with after-tax savings. With tax rates likely to rise over the coming decades, having a tax-free bucket in retirement is one of the most durable financial advantages you can give a child.

My Kids' Policies: Real Numbers

Both of my children have Allianz IUL policies. My son's was started at age 8, my daughter's at age 5. Because she's younger and female — both of which lower the cost of insurance — I was able to fund her policy at a lower premium while targeting nearly identical retirement income. Both illustrations were run at a 6.65% assumed rate of return — a conservative projection. Given the participation rates, multiplier bonuses, and uncapped index strategies on these policies, I fully expect actual performance to outpace these numbers. The 2026 index credits below show exactly why.

My Son's Policy — Age 8, Male

Annual premium of $3,420 with an initial death benefit of $121,019. Below are the projected cash values and retirement income from his Allianz illustration.

| Milestone | Projected Value |

|---|---|

| Initial Death Benefit | $121,019 |

| Cash Value at Age 40 | $359,455 |

| Cash Value at Age 50 | $779,922 |

| Cash Value at Age 65 | $2,381,391 |

| Tax-Free Income (Ages 65–120) | $210,366/year |

My Daughter's Policy — Age 5, Female

Annual premium of $2,750. Lower cost, slightly more favorable gender rates, and two additional years of compounding put her projections fractionally ahead of her brother's despite the lower premium.

| Milestone | Projected Value |

|---|---|

| Cash Value at Age 40 | $372,535 |

| Cash Value at Age 50 | $806,645 |

| Cash Value at Age 65 | $2,461,000+ |

| Tax-Free Income (Ages 65–120) | $222,070/year |

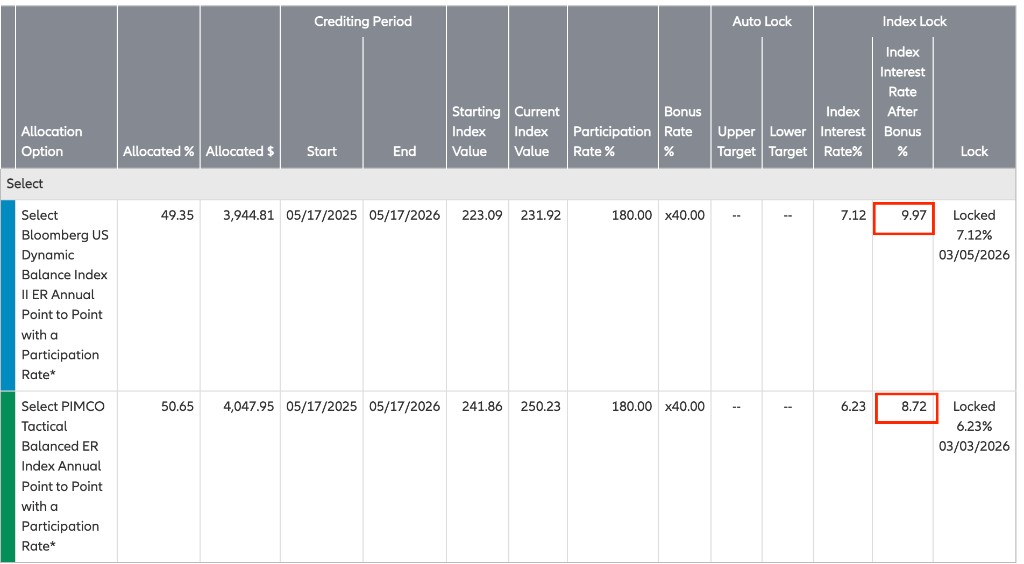

2026 Index Returns: My Son's Policy

One of the features I specifically chose Allianz for is their rate lock. Most IUL carriers credit your index return at the end of the annual point-to-point segment — you don't know your rate until the period closes. Allianz lets you lock your credited rate mid-segment and guarantee it for the full year, even if the index moves against you before the period ends.

In early March 2026, I could see the market was showing signs of a pullback. I locked both of my son's index segments before it happened. His new crediting period starts May 17, 2026, and these rates are already guaranteed regardless of where the market goes between now and then.

| Index | Base Rate | With Bonus & Participation | Locked |

|---|---|---|---|

| Bloomberg US Dynamic Balance II ER | 7.12% | 9.97% | March 5, 2026 |

| PIMCO Tactical Balanced ER | 6.23% | 8.72% | March 3, 2026 |

Both segments run May 17, 2025 through May 17, 2026. His cash value will be credited both of those rates when the period closes — regardless of market conditions between now and then.

Expert Tip: The Rate Lock Advantage

The rate lock is one of the most underappreciated features in IUL design. It converts an annual point-to-point strategy — which normally forces you to ride out full-year volatility — into something you can actively manage. Most agents don't even mention it. I use it on my own kids' policies.

-Brad Cummins, Insurance Geek FounderWhy I Chose a Kids IUL Over a Roth, 529, or UGMA

When I was deciding how to build wealth for my kids, I looked at all four options. Here's why none of the alternatives made the cut.

The Tax Advantages Aren't Even Close

A 529 gives you a state income tax deduction going in, but it taxes you on the way out if the money isn't used for qualifying education expenses. A UGMA transfers to your child at 18 or 21 and is subject to capital gains tax. A Roth IRA has tax-free growth — but your child needs earned income to contribute, which made it completely off the table when I started these policies. My son was eight. My daughter was five. Neither had a W-2.

An IUL grows tax-deferred and the cash value comes out through policy loans — which the IRS doesn't treat as income. No taxes going in, no taxes coming out, no income requirement, no age restriction.

I Never Wanted to Risk Losing Their Money

A Roth IRA or UGMA invested in the market is fully exposed to downside. A bad sequence of returns in the years before your child needs the money can wipe out a decade of growth. I wasn't willing to take that risk with my kids' policies.

The 0% floor on an IUL means the worst year my son or daughter can have is zero — they keep every gain they've ever earned. I locked in nearly 10% on his Bloomberg segment and 8.72% on PIMCO in March 2026, right before the market pulled back. That's what the floor protection actually looks like in practice: gains locked, losses impossible.

Liquidity With No Strings Attached

A 529 restricts funds to education. A Roth IRA locks contributions until 59½ unless you want penalties and taxes on earnings. A UGMA hands full control to your child the moment they turn 18 — whether they're ready for it or not.

An IUL has none of those constraints. My kids can access their cash value at any age for any purpose — college, a business, a down payment, or simply leaving it alone until retirement. There's no penalty for using it early and no requirement to use it at all. That flexibility matters because life doesn't follow the plan you made when your kid was in diapers.

Frequently Asked Questions

Index Universal Life

Kids IUL is design and funding. Get a realistic illustration and we’ll walk it line-by-line.

Get an illustration

About Brad Cummins

Brad Cummins is the founder of Insurance Geek and primary author of its educational content. Licensed since 2004, he brings over 21 years of experience structuring life insurance and IUL strategies for clients nationwide.

Fact checked by Ryan Wood

Ryan Wood is a licensed insurance professional and contributing advisor at Insurance Geek, serving as a fact checker and technical reviewer for life insurance and annuity content. First licensed in 2013, he brings more than 12 years of experience and holds licenses in over 40 U.S. states.