Home Insurance

Your home is more than a house. Protect what matters most.

Expert articles on homeowners insurance coverage, costs, discounts, and claims. Find the right policy to protect your home and everything in it.

What is home insurance?

Home insurance (also called homeowners insurance) protects your home, belongings, and finances from covered perils like fire, theft, and liability claims. A standard policy typically includes four core coverage types: dwelling coverage (the structure), personal property (your belongings), liability (injuries or damage you cause), and loss of use (temporary living expenses if your home is uninhabitable).

What does home insurance cover?

What home insurance typically does NOT cover

- Flood (requires separate flood insurance)

- Earthquake (requires separate earthquake policy)

- Normal wear and tear

- Pest infestations (termites, rodents)

- Intentional damage

Types of home insurance policies (HO-1 through HO-8)

| Policy | Description |

|---|---|

| HO-1 | Basic form — limited named perils |

| HO-2 | Broad form — more named perils than HO-1 |

| HO-3 | Special form — most common; open perils on dwelling, named perils on contents |

| HO-4 | Renters insurance — covers personal property only |

| HO-5 | Comprehensive form — open perils on dwelling and contents |

| HO-6 | Condo insurance — covers unit and improvements |

| HO-7 | Mobile home insurance |

| HO-8 | Modified coverage — for older homes with replacement cost limits |

| DP-3 | Dwelling fire / landlord — rental property you own but do not occupy |

Renting out a property you own? See landlord insurance for dwelling fire (DP-3) and rental-property coverage—not an HO-3 on a home you do not occupy.

How much does home insurance cost?

The average cost of home insurance in the U.S. ranges from about $1,500 to $2,200 per year, depending on your location, home value, and coverage choices. Factors that affect your rate include your home's rebuild cost, deductible, claims history, and discounts you qualify for.

Learn more about home insurance costs →Home insurance discounts

- •Bundling — Combine home and auto for 10–25% off

- •Security systems — Burglar alarms, smoke detectors

- •New home — Newer construction often qualifies for discounts

- •Claim-free history — No claims in recent years

- •Loyalty — Some carriers offer discounts for long-term customers

Coverage components

Dwelling Coverage (Coverage A)

Your home's rebuild cost is not the same as its market value. Learn how Coverage A should be sized before a claim.

Learn more →Personal Property Coverage (Coverage C)

Belongings coverage looks simple until depreciation and limits apply. See how to protect the items you would actually replace.

Learn more →Liability Coverage (Coverage E)

Liability claims can reach beyond the house itself. See what Coverage E does and when higher limits make sense.

Learn more →Loss of Use Coverage

A covered claim can force you out before repairs are done. Learn how loss of use keeps temporary living costs from piling up.

Learn more →Home Insurance Perils

A policy can cover one cause of loss and exclude another that looks similar. See how perils decide whether a claim pays.

Learn more →Home Insurance Claims

How to file and manage a claim.

Top Home Insurance Companies

The cheapest home carrier is not always the best fit. See how coverage, claims, and local risk should shape the choice.

Learn more →Landlord Insurance

A homeowners policy on a rental rarely survives a claim. See what landlord and dwelling fire coverage actually protects.

Learn more →Landlord Insurance Cost

Most single-family rentals run $800–$1,500 per year. See what drives the price and how bundled vs monoline carriers compare.

Learn more →Does Home Insurance Cover Rentals?

Renting out a home without updating the policy is the most common path to a denied claim. See why the HO-3 fails and what replaces it.

Learn more →Home insurance guides

Why choose Insurance Geek for home insurance?

Rate Watch

Save more over time without re-shopping. Rate Watch notifies you every renewal if your rate increases and there are better offers — so you don't have to remember to shop again.

Insurance Geek Wallet

All your policies in one place. The Insurance Geek Wallet stores policies from any carrier in one app — so you know what you have, when it renews, and never hunt for a document again. (Coming soon)

Expert guidance

Start online, finish with a licensed agent. Get digital convenience plus human expertise before you bind — so you're confident in your choice.

What Our Customers Say

How to get home insurance

Start your quote

Use our quote widget above or click Get a Quote. Enter your basic information and we'll shop multiple top carriers for you.

Pick coverage amount and policy type

Choose how much dwelling coverage you need and which policy type fits you — HO-3, HO-5, or another option.

Apply

Apply directly on our site. Complete the application.

Pay first premium and accept policy

Review your offer, pay your first premium online, and accept your policy to activate coverage.

Home insurance by state

Home insurance FAQs

Our hub content is written and reviewed by licensed agents. About our experts · Editorial standards

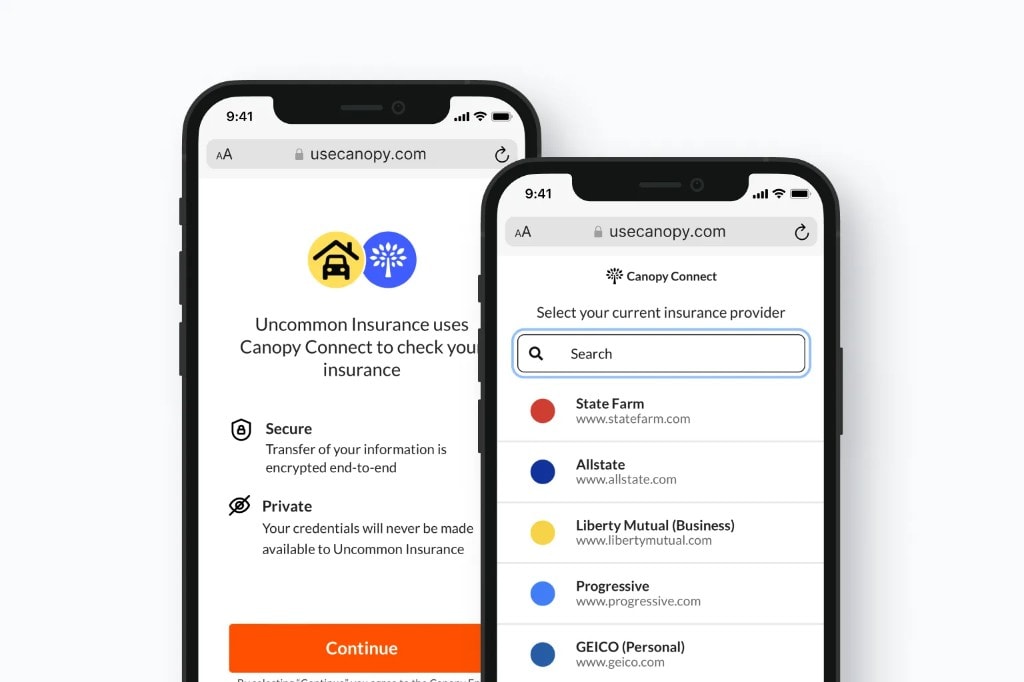

Don’t have time to run a quote? Just send us your policy.

Share your current declarations page with us in two clicks. Takes about 30 seconds. We'll review your coverage, check for gaps, and compare our carriers to your current policy.

Connect your policy