Our editorial team follows strict guidelines to ensure accuracy and objectivity. Learn more about our process.

How Our Home Insurance Calculator Works

Our home insurance calculator is the fastest and easiest way to compare and estimate multiple home insurance quotes at one time. You can try it for free and find the average home insurance cost easier and faster than ever.

Estimate Your Quotes Right Away

Our homeowners insurance calculator will send an API rate call to each insurance company that integrates with Insurance Geek. Currently, we have multiple carriers to compare in each state and more integrations are being built.

Getting the Dwelling Reconstruction Cost

Every carrier has a different method for calculating your reconstruction dwelling coverage limit. How much coverage you need can vary, and we can talk with you about how to do an assessment based on the cost of materials and labor in your area.

How does our calculator get the reconstruction cost value?

We send the construction details entered on our quote form to all the home insurance carriers, then each company will calculate and estimate the reconstruction cost then send back each's own dwelling coverage limits. Each carrier will require you to carry 100% replacement cost coverage on the dwelling.

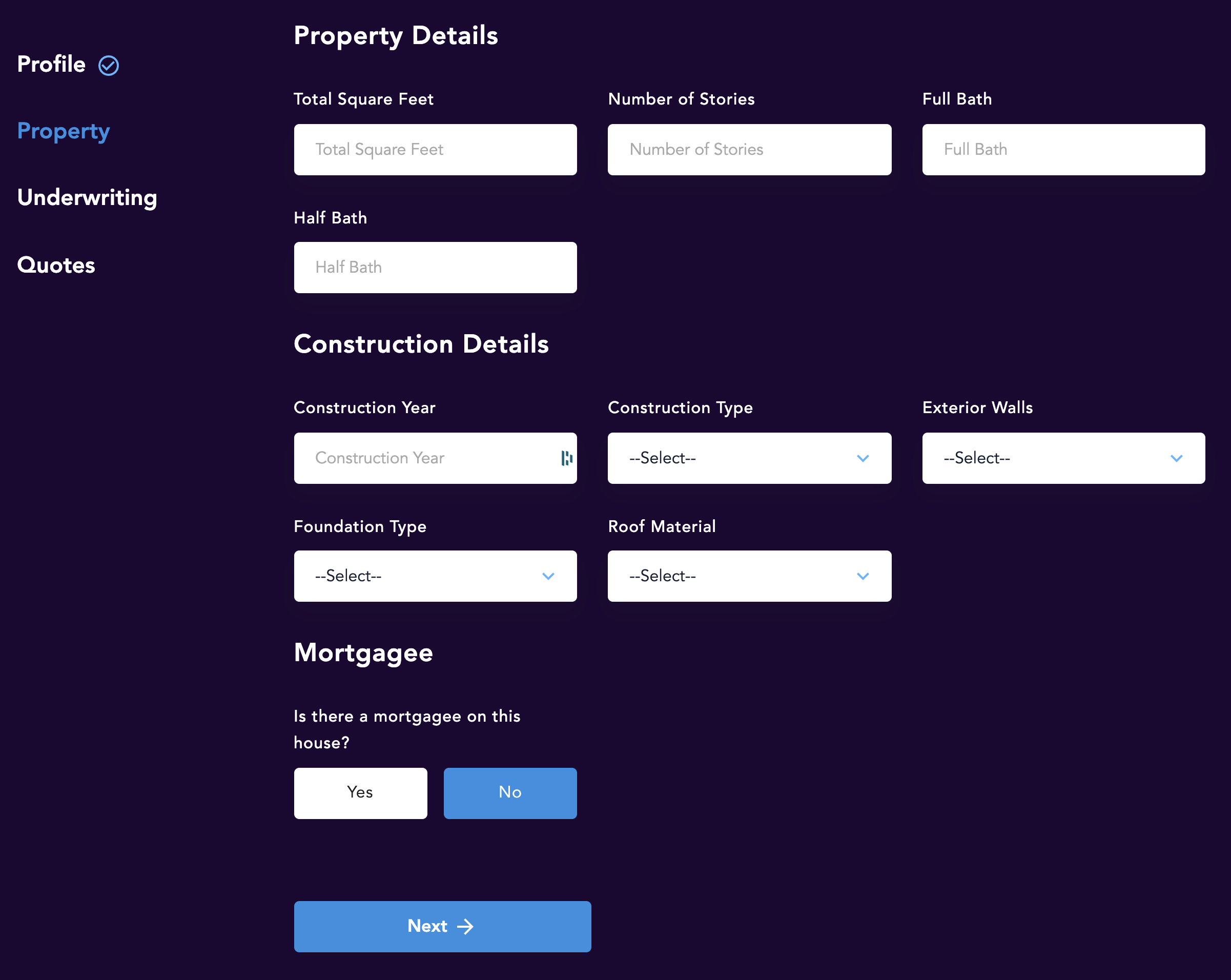

Some of the parameters to get a reconstruction cost to consist of:

Property Details:

- Total Square Feet

- Number of Stories

- Total Full Bath

- Total Half Bath

- Construction Year

- Construction Type

- Exterior Walls

- Foundation Type

Personal Property Calculation

Each insurance company will return values in our calculator with either 50 or 75% of your dwelling value. So your personal property will be a % of the reconstruction cost the carrier returns, you can increase this figure if you feel there is not enough personal property coverage.

Insurance Geek's Home insurance calculator FAQs

In just three steps our calculator will show you homeowners insurance rates from multiple carriers at once.

How long does a quote take?

You can complete our entire quote form in about 60 seconds. It will calculate home insurance rates in real-time and show multiple home insurance company's cost at once.

What type of questions do we ask on the calculator?

It's a simple 4 step form. We ask your basic personal data, the property data, some underwriting questions and then you get the quote results.

How many carriers quotes will I see in the calculator?

We have multiple carriers who are in our homeowners insurance cost calculator. The carrier you will see depends on your state. There are a few states where we do not have carriers like Hawaii, Florida, and Alaska.

Will I get instant real-time quotes?

Yes, as long as we have a carrier in your area who will write a policy you will see home insurance premiums displayed.

How to recalculate your coverages?

Once you see the homeowners insurance premiums from each carrier you can hit the edit button to adjust or add more coverage and increase limits on things like liability insurance.

Home insurance and personal property coverage

Homeowners insurance covers a wide range of possibilities, regarding potential damage or loss related to your residency.

Dwelling coverage: This pertains to the actual structural integrity of your home. You will need to know the cost of repairing or rebuilding your house in order to have enough dwelling coverage.

Liability coverage: Often used when talking about auto insurance, liability, in this case, refers to situations where you cause any kind of damage to someone else.

Personal property coverage: This simply refers to your belongings, in case of a robbery or accident. Personal property coverage helps to pay for, or replace, lost items.

Medical payments coverage: Applies to any injury someone might suffer in your home during a covered loss.

Additional living expenses: Should something happen to your home and you have to find temporary housing - the additional expenses you may deal with are covered. This strictly goes for expenditures beyond your established spending norm.

Weather-related risks: While 'weather -related risks' are listed, home insurance coverage doesn't include natural disasters like floods or earthquakes. These require additional insurance.

There are many factors to consider when estimating home insurance costs:

- Location

- Personal information (history of claims, credit score)

- Deductibles

- The home's value (how much it would cost to rebuild it)

- Personal property value (belongings)

- Possible environmental hazards

- Details of the house (age, construction, custom features, style)

- Other structures and additional features (sheds, pools, tree houses, countertops)

Location is a huge thing for insurance companies. They can use the information you give them to come up with a quote.

How does location help exactly?

Based on the area or zip code, the insurance carrier will collect information on the average value of other homes in the neighborhood.

They will also examine local building costs, the number of claims that have been filed in that area as well as other factors.

In other words, if there is a lot of crime in the area you wish to inhabit, your insurance carrier will naturally charge you more, as the risk of robbery, theft, or property damage is high.

Homeowners insurance costs can increase as time goes on, as you may have guessed. This is of course in part due to the ever-changing environment and economic factors. But it also has to do with our very own homes.

As they age over time, their structural integrity can weaken, which can have an effect on your structure's coverage.

Because of this, you may want to revisit your financial protection plan, or make changes to some of the policy limits you've established.

States with low average home insurance rates

A very popular topic indeed.

I've covered the most and least expensive home insurance states. You'll be able to see examples of how environmental risk - or lack thereof - can influence the average cost of owning a home.

Insurance deductibles

A deductible is what you pay for a covered claim before your insurance kicks in. In other words, out-of-pocket costs.

You and your carrier determine just how much coverage is going to be provided. This sets a threshold for your homeowners policy.

Now, if the cost of damage you happen to receive falls below that threshold, it's you who pays for the repairs, not the insurance companies. They only get involved once the threshold has been crossed.

Let's look at an example:

A horrible storm happened while you were on vacation. Your home has ended up with broken windows, the kitchen is ruined and the roof's had a good deal done to it. Maybe you even lost some personal belongings.

On top of all that, you asked your friend to watch over the house and they got injured.

Let's say you've settled on a $2000 deductible. If the total damage caused by the storm is evaluated to be around $1500, you'd have to pay for the repairs yourself.

If, however, it turns out to be around $2100 or higher, that's when the carrier steps in.

The cost to rebuild the windows, kitchen, and roof would be settled by the dwelling coverage. You would be reimbursed for the lost belongings thanks to personal property coverage.

Lastly, your friend's medical expenses could be paid for through liability coverage.

How high should your deductible be?

There's a give-and-take, but it's simple.

A high deductible means that the damage done to your home would have to be pretty drastic for the insurance to cover it. But at the same time, it lowers your home insurance premium.

Have a detailed insight into your personal finance, and go over possible outcomes with your insurance agent.

That's going to make it easier to decide on a deductible and come out with a manageable home insurance rate.

Are homeowners premiums paid yearly or monthly?

There's a variety of options. Your carrier's insurance policy might allow for monthly payments or even annual. It also depends on whether you have a mortgage on your home or not.

Some carriers would require yearly escrows, which they will pay the home insurance premium in full once a year. Going with this route and paying in full can even have benefits in the form of discounts.

If you're a tenant, not a homeowner

If you happen to be renting a house, obviously you're not able to attain any dwelling coverage yourself. This is where renters insurance comes in.

Renters insurance, as stated, doesn't come with dwelling coverage, but it's good to have if you're not a homeowner at the moment.

Estimate your home insurance cost today

We at Insurance Geek have gone through what you're probably going through right now.

Dwelling coverage, coverage limits, the average cost of home insurance, and dozens of other factors can pile up and block any productive action.

That's exactly why we want to give you everything you need right away.

With multiple carriers in nearly every state, you get multiple home insurance quotes in real-time.

Contact us for any help you need or calculate your rates online with us today! We're committed to building personalized policies that satisfy all your needs.

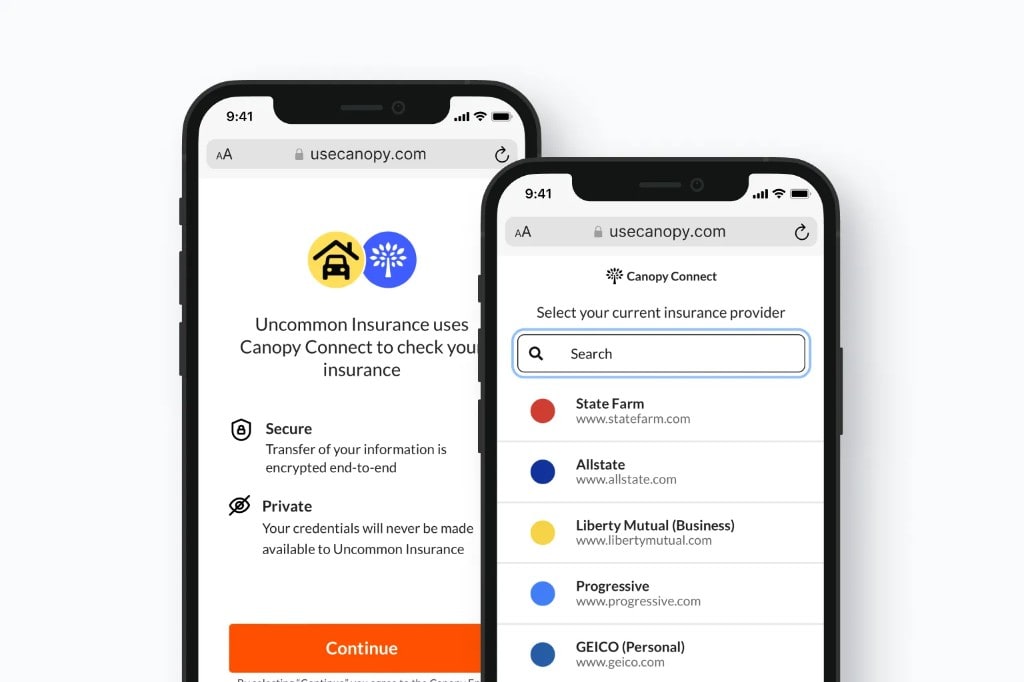

We pull your declarations page, then price it with our carriers

You connect your existing insurance account through our secure Canopy link. That imports your declarations page—dwelling limit, deductibles, endorsements—not a stripped-down quote form. We use that snapshot to quote the same coverage stack with our appointed carriers, call out where you’re underinsured, and show whether another carrier beats your renewal for equivalent protection.

Don't have time to run a quote? Just send us your policy

Share your current policy declarations pages with us in two clicks. Takes about 30 seconds. We'll review your coverage, find gaps, and compare our carriers to your current policy.

Connect your policy

About Brad Cummins

Brad Cummins is the founder of Insurance Geek and primary author of its educational content. Licensed since 2004, he brings over 21 years of experience structuring life insurance and IUL strategies for clients nationwide.

Fact checked by Brianna Baiocco

Brianna Baiocco runs P&C operations at Insurance Geek and fact-checks property and casualty content. Licensed since 2009, she brings over 16 years of experience in auto, home, renters, and commercial insurance.