Our editorial team follows strict guidelines to ensure accuracy and objectivity. Learn more about our process.

We built this list for shoppers who want recognizable carriers that show up in real comparison shopping—not a grab bag of niche apps. Below: a tight table, six ranked reviews, and an honorable mention for a newer name worth watching.

Why this list (and how we ranked)

You’ll get a comparison table plus a short review for each pick. We weighted A.M. Best financial strength, coverage breadth and endorsements, bundling value, claims and service signals, and how easy the carrier is to buy and service in the real world. Rankings are educational—your best fit still depends on state, underwriting, and your exact home.

Quick Comparison Table

| Home insurance carrier | Insurance Geek rating | A.M. Best | Best for |

|---|---|---|---|

| Nationwide Insurance | 8/10 | A+ | Overall value & bundling |

| Travelers Insurance | 8.5/10 | A++ | National scale & claims reputation |

| Liberty Mutual, formerly Safeco | 8/10 | A | Equipment breakdown; Safeco brand retires Apr 2026 |

| Chubb Insurance | 8/10 | A++ | High-value homes & luxury |

| Cincinnati Insurance | 8/10 | A+ | Custom endorsements & agent design |

| The Hartford | 8/10 | A+ | AARP-endorsed program recognition |

Top 6 Home Insurance Companies

Rank 1: 1. Nationwide Insurance

- Our rating

- 8/10

- A.M. Best

- A+

- Best for

- Overall value & bundling

- Fortune 100 carrier with home, auto, life, and pet products

- Solid HO foundation: dwelling, liability, loss of use, ordinance

- Brand New Belongings®, Better Roof Replacement®, Valuables Plus®

- Multi-policy discounts when you bundle home with auto or other lines

Nationwide stays in our top tier for homeowners who want one carrier to handle multiple lines without giving up useful endorsements. Expect strong standard protections plus practical add-ons for water backup, identity theft, and extra rebuild cushion after a major loss. If bundling home with auto (or life/pet) is part of your plan, Nationwide’s multi-policy story is often where the math gets compelling.

Best for: Households that want broad access, strong bundling, and a familiar national footprint. Consider: Total price still varies by state—run apples-to-apples quotes.

Rank 2: 2. Travelers Insurance

- Our rating

- 8.5/10

- A.M. Best

- A++

- Best for

- Scale & stability

- Large national personal-lines footprint and long operating history

- Broad coverage options and bundling with auto and other lines

- Strong financial strength (A.M. Best A++ on key insurance entities)

- A frequent “short list” name in third-party homeowner satisfaction studies

Travelers belongs on a 2026 best-companies page because it matches what most searchers expect from the category: a major carrier with deep capacity, broad availability, and a claims operation that gets discussed constantly in consumer rankings. It’s not the flashiest brand on social media—it’s the kind of pick homeowners make when they want stability and a policy stack that behaves predictably when something goes wrong.

Best for: Mainstream homes where you want a household-name insurer with strong financials. Consider: Your best Travelers bundle still depends on local pricing—compare against Liberty Mutual and Nationwide on identical limits.

Rank 3: 3. Liberty Mutual, formerly Safeco

- Our rating

- 8/10

- A.M. Best

- A

- Best for

- Systems & endorsements

- Liberty Mutual is sunsetting the Safeco name (target: Apr 25, 2026)—coverage and claims continue

- Equipment breakdown coverage for many budgets

- Guaranteed Repair Network with American Home Shield tie-in

- Online claims plus multi-line discounts (auto, RV, and more)

Liberty Mutual is retiring the Safeco brand for personal lines (including home), with a widely discussed target of April 25, 2026. Practically, you may see Liberty Mutual branding on quotes and ID cards even when you’re buying the same independent-agent personal-lines products shoppers knew as Safeco. Underwriting entities and coverages are not “reset” because of a logo change—still read your declarations page at renewal.

The product story here is still equipment breakdown and flexible endorsements for real homes—not just fire and wind, but systems that fail when you’re not expecting it.

Best for: Homeowners who want affordable systems protection and strong optional coverage through the independent channel. Consider: Availability varies by state—confirm forms and endorsements with your agent.

Rank 4: 4. Chubb Insurance

- Our rating

- 8/10

- A.M. Best

- A++

- Best for

- High-net-worth homes

- Extended replacement cost and replacement-cost contents

- Scheduled jewelry, art, wine, and collectibles programs

- Cyber, umbrella, and domestic-staff liability options

- Concierge-style claims and risk services

Chubb is the luxury lane: higher limits, higher expectations, and higher-touch service for larger homes and more complex asset pictures. If you have scheduled valuables, a bigger liability footprint, or you want rebuild coverage that behaves like premium insurance, Chubb is the usual benchmark.

Best for: High-value homes, collections, and households that need liability depth. Consider: Premium pricing—make sure the fit matches the need.

Rank 5: 5. Cincinnati Insurance

- Our rating

- 8/10

- A.M. Best

- A+

- Best for

- Tailored coverage

- Executive Classic™ and Capstone endorsement suites

- Guaranteed replacement cost up to 25% above dwelling limit

- Rental-property, water backup, and cyber options

- Decades of stable ratings and agent-led design

Cincinnati fits when your home doesn’t match a cookie-cutter quote: older construction, rental exposure, water-backup worry, or a preference for layered endorsement packages. The win is agent-led design—if your agent knows the menu, you can build a policy that actually matches the risk.

Best for: Custom policy design with strong financial ratings. Consider: The outcome depends heavily on agent expertise.

Rank 6: 6. The Hartford

- Our rating

- 8/10

- A.M. Best

- A+

- Best for

- AARP program & mature homeowners

- Widely recognized homeowners program endorsed by AARP

- Strong financial ratings on key underwriting members

- A common short-list carrier for shoppers comparing national brands

- Bundling and standard HO options competitive in many markets

The Hartford earns a spot here for the same reason other national incumbents do: distribution scale, recognizable branding, and a homeowners product that’s often in the conversation for mature homeowners—especially through the AARP-endorsed program many shoppers explicitly search for. It’s not insurtech novelty; it’s a traditional carrier pick when you want a familiar name on the dec page.

Best for: Shoppers comparing household-name carriers and those interested in AARP-endorsed homeowners options. Consider: Program eligibility and packaging rules vary—confirm details with your agent or the carrier.

Honorable mention: Branch Insurance (new & upcoming)

Branch isn’t in our core six because we treat “best of breed” on this page as decades-deep national scale and a claims track record that’s easy to benchmark side-by-side with Travelers-style incumbents. Branch is still worth a mention: it’s a newer distribution story built around bundled simplicity and a cleaner buying experience for shoppers who hate stacked endorsements they can’t decode.

If you’re early in your search and want a fast bundle quote, Branch can be a useful comparison point—just treat it like a rising option to validate against the core carriers above, not a default replacement for them.

Expert tips

Expert Tip: Maximum home insurance savings

Bundling and quoting apples-to-apples (same deductibles, replacement-cost assumptions, and liability limits) usually beats chasing gimmicks. Smart-home discounts and roof upgrades can help—but the big levers are shopping correctly and not buying “cheap” that secretly strips coverage.

—Brad Cummins, Insurance Geek Founder

Expert Tip: Understanding policy comparison

Price matters, but the winning quote is often the one with better coverage terms for a small premium difference—especially in wind- and hail-heavy markets.

—Ryan Wood, Licensed Insurance Agent

Quick coverage checklist

Open perils vs named perils: HO5-style open peril covers everything not excluded; named peril only lists what’s covered—verify what you actually bought. RCV vs ACV: replacement cost on the dwelling is the usual target for owner-occupied homes; ACV can leave you short after a big loss. Remember A–F (dwelling, other structures, personal property, loss of use, liability, guest medical)—if any line looks randomly low, fix it before bind. Premium drivers include credit-based insurance scoring (where allowed), claims history, roof age, catastrophe exposure, and discounts for security or mitigation.

The right carrier depends on your state, your home's profile, and whether bundling or endorsements matter more to your situation. As a licensed independent agency appointed with several of the carriers on this list, we can compare real quotes side-by-side and help you find the combination of coverage and price that actually works for your home — not just the one with the biggest ad spend.

Shopping the carriers above is easier when you can see real pricing for your home and renewal window in one place. Our team matches coverage limits and deductibles so you are comparing like-for-like offers. Get homeowners insurance quotes when you are ready to see numbers you can actually move forward with.

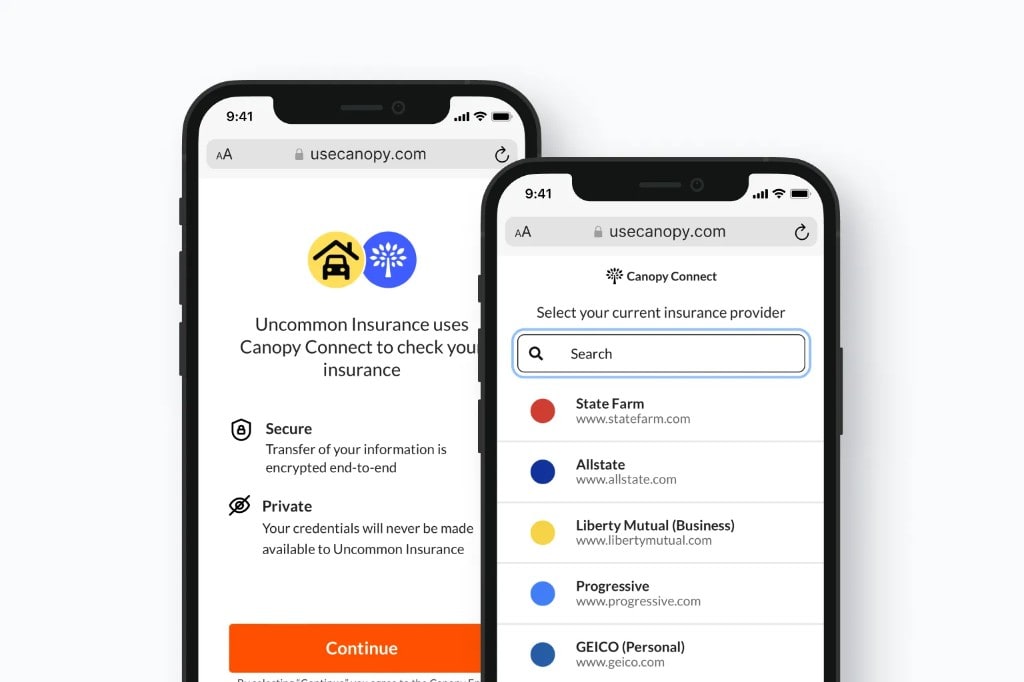

Don't have time to run a quote? Just send us your policy

Share your current policy declarations pages with us in two clicks. Takes about 30 seconds. We'll review your coverage, find gaps, and compare our carriers to your current policy.

Connect your policy

Frequently Asked Questions

Secure your personalized home insurance quote today

Run quotes and let a licensed agent help you pick the carrier that fits—not the one with the loudest ad budget.

Bundling home and auto (and sometimes life) remains one of the simplest ways to reduce total spend when your carrier is competitive on both lines.

Find your perfect home insurance match

Insurance Geek is appointed with roughly half of the national carriers featured in this guide and can shop quotes across that panel for you. We also place coverage with specialty, regional, and program markets when they are the better fit—examples you may see alongside the big names include Branch, Openly, and Assurant (availability varies by state, product, and underwriting rules).

About Brad Cummins

Brad Cummins is the founder of Insurance Geek and primary author of its educational content. Licensed since 2004, he brings over 21 years of experience structuring life insurance and IUL strategies for clients nationwide.

Fact checked by Brianna Baiocco

Brianna Baiocco runs P&C operations at Insurance Geek and fact-checks property and casualty content. Licensed since 2009, she brings over 16 years of experience in auto, home, renters, and commercial insurance.